Forbes, one of the few business magazines that actually takes a look at the business of sports, has just released its yearly ranking of NBA franchises by total valuation.

The NBA's Most Valuable Teams | Forbes

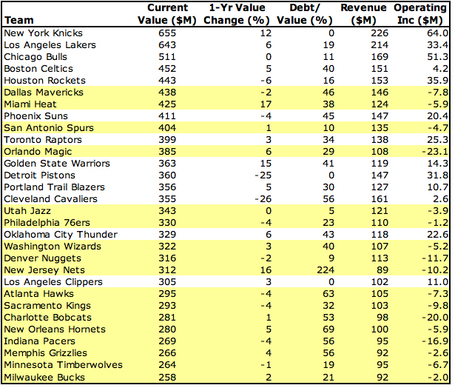

Here is a snapshot of all the teams' valuations, ranked from most valuable to the least:

Source: Forbes.com

For more analysis and some helpful charts, please check out the Detroit Pistons blog "PistonPowered", where the author gives you some easy visuals to follow.

Illustrating the Pistons' Fall in Forbes NBA Franchise Value Projections | PistonPowered

A few brief comments:

- Teams that have lost money (negative operating income) are highlighted in yellow.

- The Knicks and Lakers swapped spots from a year ago, in part I'm sure due to the addition of Amare Stoudemire and increased ticket sales. The Bulls finished a distant third, but these three represent the three largest NBA markets.

- The Thunder, despite being only ranked 18th in total value, rank 6th in operating income.

- Only 13 teams made money last year, which gives credence to Stern's claim about how many franchises are struggling.

- Only three teams are carrying zero debt - the Knicks, the Pistons, and the Clippers. Since the Pistons are on the market for sale, I would think that this number would make them more attractive than the Warriors, who are also on the market.

- The particularly staggering number to me is the debt/value ratio. If you're not familiar with this financial ratio, what this number tells you is how much borrowed money the team is using to finance its assets. It is also sometimes called a leverage ratio. The advantage to using debt is that it requires less out of your pocket up front, so you can create larger business opportunities with less cash on hand (hence the term "leverage" - it acts like a lever, moving large things with minimal effort). Conversely, the more debt you use to finance your operations, the less you get to put in your pocket. This is because when you use debt, you have to pay the debtor for borrowing his money; just like if you took out a loan from the bank, you'd be charged interest on it as a way of compensating the bank for taking the risk of lending to you.

What alarms me most about the seemingly high debt/value numbers is that it exposes the team to extra risk in economic downturns. This is because when things go sour, companies can always choose to pay themselves less (i.e. reduce salaries, benefits, etc) but companies cannot choose not to pay their debt interest. To do so would cause the team to default on its loans, and there are significant consequences to such an act.

(One interesting caveat to which I don't know the answer - I don't know how guaranteed player contracts are treated in this financial structure. The player salaries are technically not debt per se, but the teams are legally obligated to pay them. Perhaps they are treated as some sort of equity hybrid, like preferred stock. If you know the answer, please fill me in)

So in reality, unless I'm misreading the story, those 13 teams that have a positive operating income could actually be making even less, because operating income is a number that has not yet been reduced by interest expense. Ergo, with teams like the Celtics and Cavaliers, who made small operating incomes, due to the debt leverage they're carrying, it may take them out of the black and into the red.

Update

After pondering the debt structure of teams, I inquired on the venerable Jeff Clark of CelticsBlog to see what he knew. He recalled that a little while back, the NBA offered some cheap loans to a number of teams, one of which was the Celtics. After doing a bit of searching, I found this story, which covers the topic:

In order to help some of the teams weather the storm, the NBA had offered unspecified types of loans to 15 teams (another of which was the Memphis Grizzlies). None of the stories go into detail as to what types of loans they were, be they bridge loans, lines of credit, long term debt, or the like. The amount was somewhere between $13-$20 million. Without knowing much more about each team's overall level of debt and equity, it is difficult to say whether this loan materially changed each accepting team's overall debt/value ratio.

Loading comments...